The Great acceleration

A New Growth Engine for a Slowing World

The global economy entered the mid-2020s facing a familiar set of structural headwinds — ageing demographics, tightening labour markets, elevated debt levels, and productivity growth that had disappointed for nearly two decades. Against this backdrop, artificial intelligence has emerged not merely as a technological novelty, but as a potential solution to the most fundamental challenge in macroeconomics: how do you grow an economy when the traditional inputs of labour and capital are increasingly constrained?

PwC's research estimates that AI has the potential to boost global economic output by up to 15 percentage points over the next decade — effectively adding one full percentage point to annual growth rates, on par with the incremental growth the world gained from 19th century industrialisation. Synovus That is not a modest claim. It places AI alongside electricity, the steam engine, and the internet as a genuine general-purpose technology — one capable of reshaping the productive capacity of entire economies, not just individual firms.

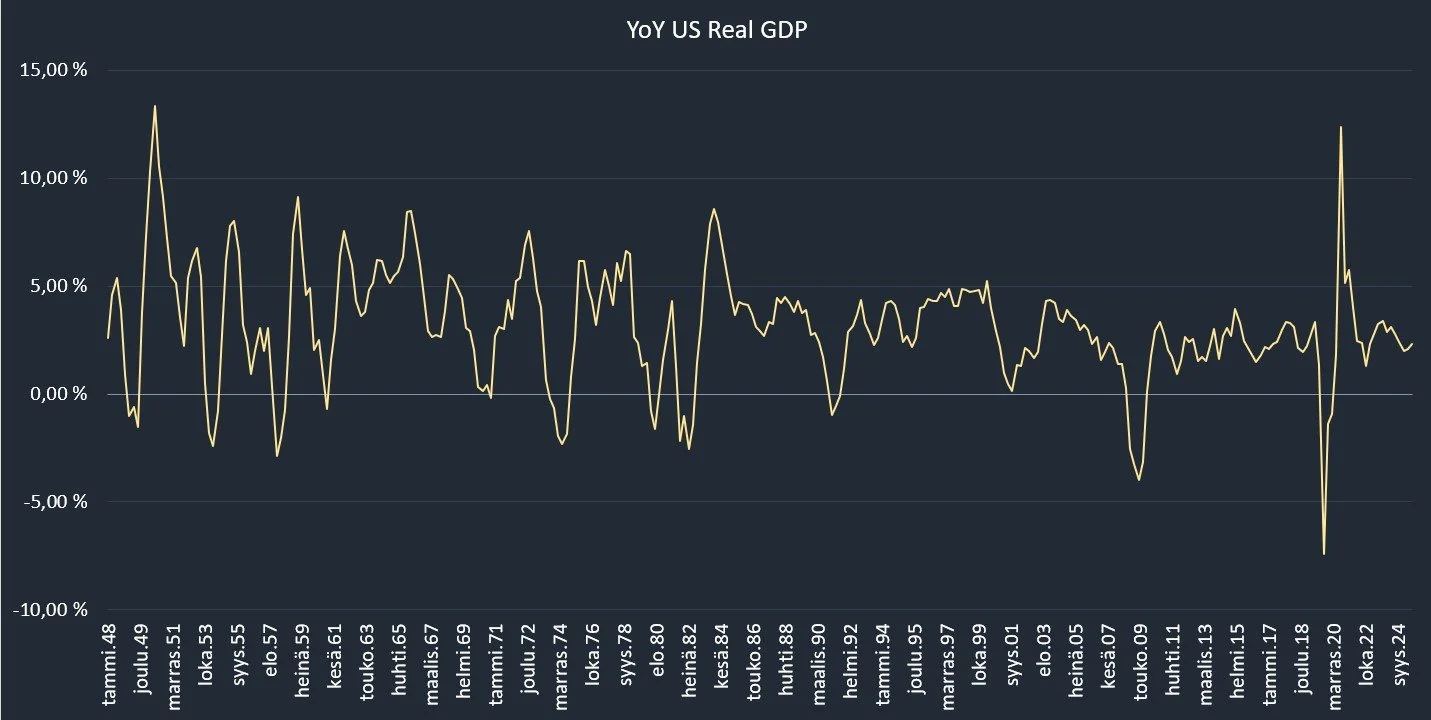

Year over year US Real GDP growth from 1948 until January 2026

The Productivity Revolution Is Already Measurable

For years, economists debated whether AI would ever translate into real productivity gains. That debate is beginning to resolve itself in the data. By late 2025, nonfarm business productivity surged by 4.9% — a figure reminiscent of the post-WWII golden age — driven by the deployment of autonomous agentic AI capable of executing multi-step business processes without constant human intervention. iQuasar

At the firm level, the evidence is equally compelling. Research across more than 500 enterprises finds that AI-driven productivity gains decompose into cost reductions accounting for 40% of the benefit, revenue growth for 35%, and accelerated innovation cycles for the remaining 25%. iQuasar These are not efficiency gains at the margins — they represent a fundamental restructuring of how value is created inside organisations. In Q1 2025, the contribution of information processing equipment to real US GDP growth surged to 0.90 percentage points — more than two standard deviations above its long-run average, surpassing even the dot-com era peak in both absolute levels and as a share of GDP. Govwin

The GDP Opportunity: A Wide Range, But Consistently Large

Experts project that by 2030, AI could contribute between $13 trillion and $19.9 trillion to global GDP, adding 1.2% to 3.5% annually through productivity gains, innovation, and entirely new markets that did not previously exist. The Birmingham Group

Academic and institutional projections vary meaningfully in their assumptions, but the direction is consistent. The Penn Wharton Budget Model estimates that AI will increase US productivity and GDP by 1.5% by 2035, rising to nearly 3% by 2055 — with 40% of current GDP in activities substantially affected by generative AI. Winvale Meanwhile, Goldman Sachs projects that AI could boost US productivity by 1.5% annually over the next decade, with measurable GDP impact beginning in 2027 iQuasar — as the current phase of infrastructure investment gives way to operational deployment at scale.

The IMF takes a similarly constructive but carefully bounded view. In its high-growth scenario, global total factor productivity increases by 1.8% within five years and 2.4% over ten years — with the most pronounced gains in AI-intensive sectors, followed by non-tradable and tradable industries. Federal News Network Importantly, the IMF also notes a risk of divergence: countries with strong AI infrastructure and skilled workforces are positioned to capture a disproportionate share of these gains, while others risk falling meaningfully behind.

The Second Wave: Beyond Digital Into the Physical Economy

The productivity gains realised thus far have been primarily digital and administrative — faster analysis, automated workflows, enhanced decision-making. But the next frontier is significantly larger. The market is preparing for a second wave: the integration of AI into physical robotics and the broader supply chain, with autonomous logistics, AI-driven manufacturing, and robotic systems beginning to reshape the physical economy in ways that extend the productivity dividend far beyond white-collar work. iQuasar

Legitimate comparisons have been drawn between this era of AI and the 1990s internet boom — both periods involved technological innovation improving overall economic productivity and increasing the long-term potential growth rates of maturing economies. Construction Dive But where the internet primarily reorganised the distribution of information, AI is reorganising the distribution of cognitive labour itself — a far broader and more structurally significant shift.

The Critical Variable: Trust and Governance

PwC's research is clear that the global growth dividend from AI is not guaranteed — it depends not only on technical success, but equally on responsible deployment, clear governance, and public and organisational trust. In scenarios characterised by lower trust and cooperation, the incremental economic boost falls to 8%, and in a pessimistic scenario, as low as 1%. Synovus

This is a critical insight that Alfred Vault takes seriously. The macro acceleration case for AI is real and well-supported — but it is not unconditional. It hinges on the world's institutions, regulators, and organisations building the governance frameworks that allow AI to be deployed at scale without triggering the kind of societal backlash that could stall adoption entirely.

Alfred Vault's View: The Growth Is Real, But Unevenly Distributed

We are genuinely optimistic about AI's capacity to drive a multi-decade macro acceleration. The productivity data is already moving in the right direction, the institutional research is directionally consistent, and the investment committed by governments and corporations globally is substantial enough to be self-reinforcing.

However, we hold two important reservations around this thesis. First, the gains will not be evenly distributed — across countries, across industries, or across companies within the same sector. The gap between organisations that genuinely implement AI and those that merely adopt the language of AI is widening, and that gap will ultimately be priced in. Second, the timeline to macro-level impact is longer than market narratives typically acknowledge — adoption friction, governance gaps, and workforce readiness remain real constraints, as we have written about separately.

Our conclusion: the AI macro acceleration is one of the most compelling structural investment themes of the coming decade — but precision matters more than exposure. Being broadly invested in "AI" is not a strategy. Identifying the specific companies, infrastructure layers, and sectors positioned to capture the productivity dividend early and durably — that is where Alfred Vault focuses its research.

This content represents the views and perspective of Alfred Vault and is provided for informational and educational purposes only. It does not constitute investment advice. Please refer to our full disclaimer.