Technology Investment Cycles

History Rhymes, But AI May Be Writing an Entirely New Verse

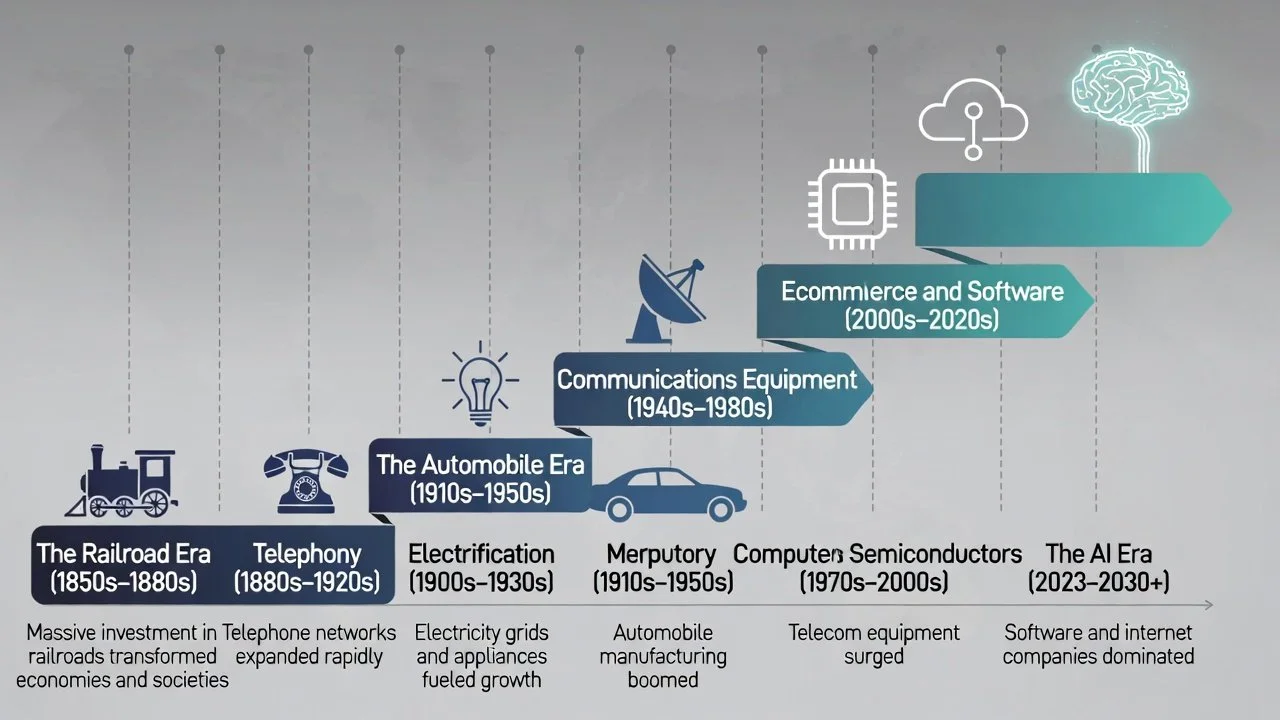

One of the most compelling visual representations of technological change comes from ARK Investment Management's Big Ideas 2026 report, which maps nearly 170 years of transformative technology investment waves — measured as capital expenditure as a percentage of GDP. What this chart reveals is both humbling and electrifying: every generation has lived through what felt like an unprecedented wave of change, and yet the current AI investment cycle dwarfs everything that came before it.

At Alfred Vault, we believe understanding these historical cycles is not merely an academic exercise — it is essential context for making sense of where we are today and what the coming decade may look like for investors.

Technology investment cycles

The Railroad Era (1850s–1880s): The First Infrastructure Boom

The railroad wave stands as the first truly transformative technology investment cycle in modern economic history, and for decades it held the record as the most capital-intensive. At its peak in the mid-1860s, railroad investment reached approximately 5% of US GDP — an almost incomprehensible commitment of national resources to a single technology. Railroads did not merely move goods and people faster — they collapsed geography, created national markets where only regional ones had existed, and enabled the industrialisation of agriculture, manufacturing, and trade. The economic multiplier was enormous, though the investment cycle itself was volatile, characterised by booms, busts, and the consolidation of countless speculative ventures into a handful of dominant operators. The lesson for investors: the technology that wins is not always the company that survives the buildout phase.

Telephony (1880s–1920s): Connecting People, Not Just Places

Overlapping with the tail end of railroad investment, telephony represented the first technology cycle built around the transmission of human communication rather than physical goods. Investment peaked at roughly 1–1.5% of GDP — far more modest than railroads in absolute terms, but structurally significant in what it enabled: the real-time coordination of business, finance, and governance across distances that had previously required days of travel. Telephony laid the groundwork for the communications infrastructure that every subsequent technology wave would depend upon, making it perhaps the most foundational — if least celebrated — of the historical cycles.

Electrification (1900s–1930s): The General Purpose Technology That Changed Everything

Electrification is the historical cycle most frequently cited by economists when drawing analogies to AI — and for good reason. At its investment peak around 1910–1920, electrification consumed roughly 1% of GDP annually, but its economic impact was orders of magnitude larger than that number implies. Electricity was a true general-purpose technology: it did not enhance one industry, it restructured all of them simultaneously. Factories, homes, transportation, communications, and medicine were all transformed. Critically, the productivity gains from electrification took decades to fully materialise — historians estimate a 30–40 year lag between widespread electrification and measurable economy-wide productivity impact. This is a pattern Alfred Vault watches closely in the context of AI adoption today.

The Automobile Era (1910s–1950s): The Consumer Technology Supercycle

The automobile investment cycle was the largest and most sustained of the pre-digital era, with capital expenditures reaching 3–4% of GDP at their peak in the 1920s. What distinguished the automobile from prior cycles was its dual nature: it was simultaneously an industrial infrastructure investment and a mass consumer product. The automobile did not just move people — it created the suburb, reshaped retail, birthed the oil industry as a geopolitical force, generated an entire ecosystem of ancillary industries from insurance to fast food, and defined the physical landscape of the 20th century American economy. The automobile wave also introduced investors to the pattern of early proliferation followed by brutal consolidation — hundreds of manufacturers in the 1910s reduced to a handful of dominant players by the 1940s.

Communications Equipment (1940s–1980s): The Invisible Infrastructure

The long wave of communications equipment investment — microwave towers, satellites, cable infrastructure, and early data networks — was less dramatic in its peaks but remarkably persistent in duration. This cycle quietly built the backbone upon which the digital revolution would eventually run. It rarely captured public imagination the way railroads or automobiles did, but its compounding effect on economic connectivity and information flow was profound. For investors, it demonstrated that the most durable returns in a technology cycle often come not from the headline innovation itself, but from the enabling infrastructure that makes widespread adoption possible.

Computers and Semiconductors (1970s–2000s): The Digital Foundation

From the 1970s through the turn of the millennium, investment in computers and semiconductors grew steadily to approximately 1.5% of GDP — a cycle that gave the world the personal computer, the microprocessor, and eventually the commercial internet. This era produced some of the greatest wealth creation events in market history, but also some of its most spectacular destructions — the dot-com boom and bust serving as a vivid reminder that even genuinely transformative technologies can become severely mispriced during their investment peaks. Crucially, the computing cycle did not end — it evolved, flowing directly into the next wave.

Ecommerce and Software (2000s–2020s): The Efficiency Revolution

The rise of ecommerce — measured in the chart primarily through warehouse investment — and the parallel expansion of enterprise software represented the maturation of the digital economy. These cycles peaked at roughly 1% of GDP each, and their defining characteristic was the dematerialisation of economic activity: the migration of commerce, communication, and business processes from physical to digital form. The companies born in this era — the platform giants of today — became the most valuable in history, not by building physical infrastructure but by building digital networks with near-zero marginal cost of scaling.

The AI Era (2023–2030+): A Cycle Without Historical Precedent

And then there is the present. What the ARK chart makes unmistakably clear is that the AI investment cycle — encompassing AI software, AI data centers, space, terrestrial infrastructure, and robotaxis — is not simply the next wave in a long sequence. It is a vertical departure from everything that came before. AI Software alone is projected to reach 8% of GDP in capital expenditure terms by 2030, with AI Data Centers adding a further 2.5% — numbers that would dwarf even the railroad era at its most capital-intensive peak.

Several factors make this cycle genuinely unprecedented. First, unlike prior technology waves which were largely sequential, the current AI cycle is simultaneously transforming every sector at once — there is no industry that AI does not touch. Second, the pace of capability improvement in AI has no historical analogue — the performance of leading models is doubling on a sub-annual basis. Third, the investment is globally distributed from the outset, with the United States, China, Europe, and the Gulf states all committing sovereign-scale capital simultaneously.

Alfred Vault's Takeaway: Position for the Infrastructure, Not Just the Hype

History teaches us several consistent lessons across these cycles. The technology that wins the buildout phase is not always the technology — or the company — that captures the long-term value. The railroad era created enormous wealth for landowners and manufacturers, not just railroad operators. Electrification's greatest beneficiaries were the factories and businesses it empowered, not always the utilities that built the grid.

At Alfred Vault, we apply this lesson directly. The AI cycle will create extraordinary value — but the distribution of that value across the investment landscape will be uneven, non-obvious, and will shift over time. Our research is focused on identifying not just who is building AI, but who is most positioned to capture the durable economic surplus it generates — in infrastructure, in applications, and in the sectors that will be structurally transformed by it.

We are, by our own assessment, in the early chapters of the longest and most consequential technology investment cycle in recorded economic history. That is not a reason for reckless optimism — it is a reason for rigorous, patient, and precise investing.

Source reference: ARK Investment Management LLC, "Big Ideas 2026: The Great Acceleration." Alfred Vault references this material for informational and educational purposes. Alfred Vault has no affiliation with or endorsement from ARK Investment Management LLC. This content does not constitute investment advice. Please refer to our full disclaimer.