Tungsten: The Invisible Metal Powering Modern Warfare and the New Critical Minerals Race

The Metal Nobody Talks About — Until They Cannot Get It

There is a metal that sits at the intersection of modern warfare, semiconductor manufacturing, and geopolitical competition — and most people have never given it a second thought. Tungsten does not carry the profile of gold, lithium, or even rare earths in mainstream investment discourse. Yet it is quietly becoming one of the most strategically significant materials in the world — and its price, its supply chain, and its geopolitical ownership structure are sending signals that Alfred Vault believes deserve serious investor attention.

Tungsten possesses the highest melting point of any element, combined with exceptional hardness, density, and electrical and thermal conductivity — properties that make it genuinely irreplaceable across a remarkable range of critical applications. iQuasar Its exceptional density of 19.35 g/cm³ — approximately 1.7 times denser than lead — enables kinetic penetration capabilities that cannot be replicated by conventional materials. CBS News When a material cannot be substituted, its strategic value compounds with every passing year of supply constraint. Tungsten is reaching that point now.

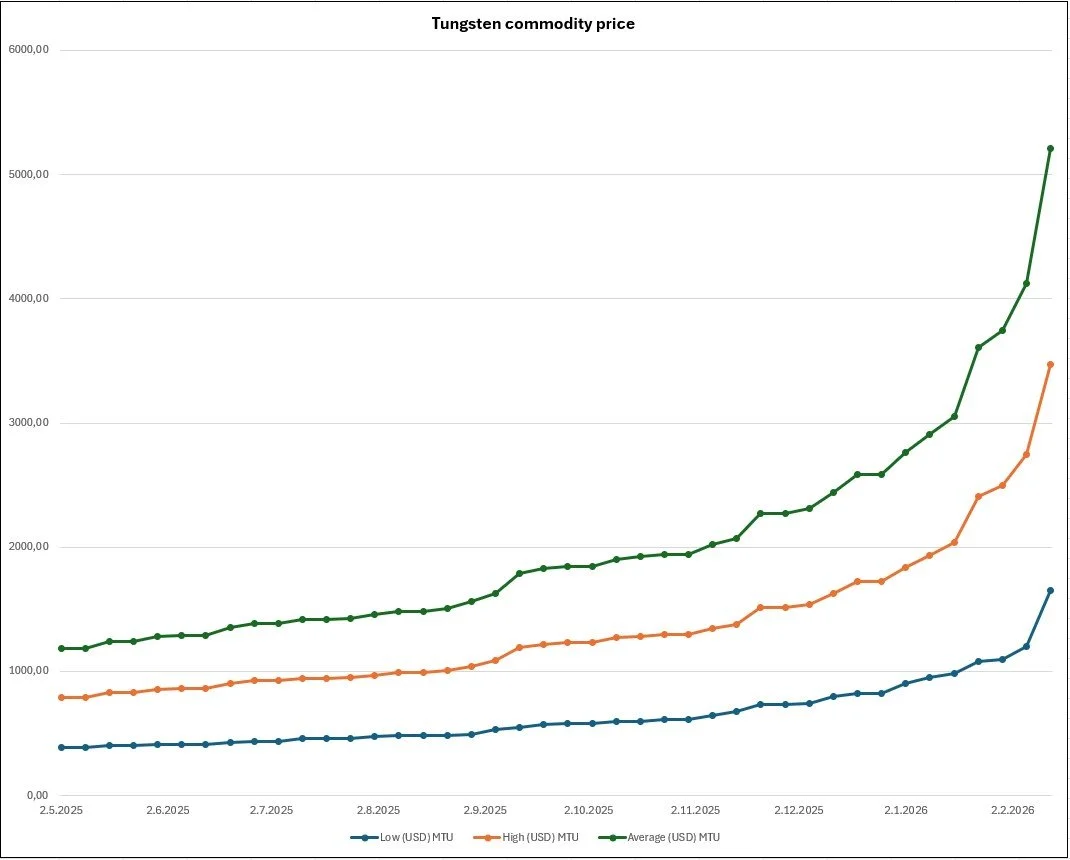

Tungsten price from May 2025 until 13th February 2026, MTU Metric Tonne Unit

The Physics of Modern Armour Penetration

To understand why tungsten matters to defence planners and procurement agencies worldwide, it helps to understand what happens in the fraction of a second when an armour-piercing round meets a hardened steel target. Penetrating modern composite armour requires a projectile of extreme density, travelling at extreme velocity, with the ability to maintain structural integrity under catastrophic stress. Tungsten fulfils this requirement better than almost any other material available.

Tungsten, usually alloyed with nickel, iron, or cobalt to form heavy alloys, is used in kinetic energy penetrators as an alternative to depleted uranium — in applications where uranium's radioactivity is problematic or where uranium's additional pyrophoric properties are not desired. Tungsten alloys have also been used in shells, grenades, and missiles to create supersonic shrapnel. iQuasar

Tungsten is used in armor plating and artillery shells because of its hardness and high-temperature resistance, enhancing the durability and effectiveness of bullet-proof vehicles, armoured tanks, and artillery parts. When used in kinetic energy penetrators, tungsten alloy projectiles can penetrate heavy armour effectively due to their sheer mass and strength — a safer alternative to depleted uranium that addresses environmental and health concerns while still providing superior performance. Winvale

The Full Spectrum of Military Applications

The military dependency on tungsten extends far beyond ammunition. Tungsten's military applications span tungsten alloy bullets and shrapnel heads, balance components in missiles and aircraft, the measuring core of armour-piercers, kinetic armour-piercers, armour and artillery shells, grenades, bullet-proof vehicles, armoured tanks, artillery parts, and rocket accessories — as well as high-speed cutting tools and super-hard moulds essential for precision weapons manufacturing. Synovus

In the most advanced munitions systems, tungsten carbide penetrator cores are used in long-rod kinetic energy penetrators for APFSDS rounds — the armour-piercing fin-stabilised discarding sabot projectiles used by main battle tanks including the Abrams, Leopard 2, and Challenger. These represent the state of the art in armour defeat technology, and tungsten is their irreplaceable core. Govwin Beyond direct munitions, tungsten carbide cutting tools are indispensable for manufacturing military equipment — shaping titanium components, armour-grade steel, and defence-grade alloys under conditions that would rapidly degrade any inferior material. Govwin

The Historical Precedent: Tungsten Has Already Decided Battles

Germany used tungsten during World War II to produce shells for anti-tank gun designs using the Gerlich squeeze bore principle, achieving very high muzzle velocity and enhanced armour penetration from comparatively small calibre and lightweight field artillery. The weapons were highly effective — but a shortage of tungsten used in the shell core, caused in part by the Wolfram Crisis, critically limited their use. iQuasar The lesson that military planners drew from this — that tungsten supply security is a strategic imperative, not a procurement detail — has never been forgotten. It is being relearned urgently today.

Artillery Production and the Scale of Current Demand

The wars of the 2020s have dramatically exposed the gap between theoretical ammunition stockpiles and the consumption rates of modern high-intensity conflict. Artillery shell consumption in the Ukraine conflict has run at rates not seen since the Second World War — with estimates suggesting tens of thousands of rounds fired per day on the most active fronts. Every armour-piercing round, every kinetic penetrator, every tungsten-tipped artillery shell that rolls off a production line requires tungsten feedstock that must be sourced, processed, and delivered.

Global military spending reached approximately $2.72 trillion in 2024 — a real increase of 9.4% over 2023, and the tenth consecutive year of growth, with a cumulative increase of 37% over the decade. European and Middle Eastern military spending growth has been particularly significant. Cambridge Currencies China's military tungsten product orders increased significantly in 2025, with demand for tungsten-based alloys including armour-piercing bullets and missile components rising sharply year-on-year. Cambridge Currencies Western defence manufacturers are simultaneously attempting to scale production — but the tungsten supply chain they depend upon runs through a single dominant supplier that has now chosen to restrict exports.

The Most Concentrated Critical Mineral Market in the World

China dominates global tungsten production, accounting for over 80% of global output. The United States ceased commercial tungsten mining in 2015 and remains heavily reliant on imports. Morgan Stanley This level of concentration — a single nation controlling more than four-fifths of global supply of a material that is genuinely irreplaceable in defence applications — represents one of the most acute strategic vulnerabilities in the Western industrial base.

Countries classified as politically unstable or extremely unstable account for 96% of tungsten supply outside China Morningstar — meaning that the diversification options available to Western buyers are limited both in scale and in reliability. The supply chain for tungsten runs through China not merely at the mining level but at the processing level: even tungsten mined in Vietnam, Portugal, or Australia typically requires Chinese intermediate processing before it reaches end-use specifications.

China's Export Controls: A Policy Tool, Not a Market Event

Effective February 4, 2025, China introduced new export controls on tungsten, along with other critical metals including tellurium, bismuth, and indium. These measures require special export permits from the Ministry of Commerce and the General Administration of Customs — replacing previous annual quota management with individual company and target country applications, creating significant bureaucratic hurdles. Morningstar

China's sequential restriction strategy demonstrates sophisticated resource diplomacy that maximises negotiating leverage while maintaining strategic flexibility. The export controls for the 2026–27 period extend restrictions beyond single-year timeframes, creating long-term supply uncertainty that forces Western companies and governments to make strategic decisions under pressure. CBS News

This is not the first time China has deployed critical mineral exports as a geopolitical instrument. The tungsten restrictions reflect a trend seen in China's past export controls on rare earths in 2010 and again in late 2024, as well as gallium and germanium in July 2023. In each case, China maintained a near-monopoly over the production or processing of these essential materials and leveraged export controls as a policy tool to enhance national security, safeguard resources, and exert geopolitical influence over Western policy. Morningstar The playbook is consistent, deliberate, and increasingly sophisticated.

The Price Explosion: A Market in Crisis

The financial consequences have been swift, severe, and — in Alfred Vault's assessment — structurally sustained rather than cyclically temporary.

Tungsten prices have tripled since early 2024, with ammonium paratungstate — the key benchmark for tungsten pricing — hitting a record $1,125 to $1,150 per metric tonne unit in China and $1,100 in Rotterdam as of February 2026, as Beijing's 2026 Catalogue of Dual-Use Items throttled exports to allied nations. CNBC

The August 2025 monthly average Chinese price for ammonium paratungstate reached $381 per mtu — up 49% year to date at that point — before surging further to $470 per mtu on September 1, representing an 83% year-to-date increase. In Europe, the August average reached $496 per mtu, a 45% increase since the start of the year. J.P. Morgan European tungsten prices have surged to their highest level since 2013. Morgan Stanley

Prices of Chinese tungsten products including concentrate, ammonium paratungstate and ferrotungsten have surged by more than 200% in 2025 according to Fastmarkets data — driven by tighter export controls, rising national security concerns, and fresh demand from the semiconductor industry. Morningstar

The supply-side picture compounds the demand shock. The average grade of tungsten ore in China has dropped from approximately 0.42% to 0.27% over the past 20 years — meaning mining one tonne of tungsten concentrate now requires processing significantly more raw ore, pushing costs higher while yields decline. J.P. Morgan China reported a 12% year-over-year decline in tungsten production in Q2 2025, while Vietnam's Nui Phao mine — one of the world's largest tungsten operations outside China — saw output fall 30% in the same quarter following environmental audits. U.S. Bank A looming 2027 deadline mandates the US military to eliminate purchases of tungsten mined or processed in China or Russia — creating a hard regulatory cliff that is accelerating emergency procurement and alternative sourcing efforts. Morgan Stanley

The Structural Case for Sustained Price Elevation

Alfred Vault views the tungsten price move not as a commodity cycle to be traded but as a structural repricing of a genuinely scarce strategic asset. Several converging forces support sustained price elevation over a multi-year horizon.

On the supply side, the development of new tungsten mines faces significant hurdles — development timelines of five to seven years, high upfront capital costs, and a thin pipeline of potential new projects after the historical price collapse between 2011 and 2015 deterred exploration investment for nearly a decade. U.S. Bank Building a tungsten mine or refinery typically takes years, followed by additional time to reach stable operations — a timeline that is incompatible with the urgency of current defence procurement needs. Morgan Stanley

On the demand side, the drivers are multiplying. Global tungsten demand is expected to exceed 130,000 tonnes in 2025 — a 6% year-on-year increase — with growth coming simultaneously from defence, semiconductor manufacturing, new energy applications including photovoltaics and EV batteries, nuclear fusion research, and traditional cutting tools. Deloitte Insights Demand for tungsten hexafluoride — a critical specialty gas used in chip manufacturing to fill microscopic contact structures in semiconductor devices — has become a key additional price driver, with semiconductor manufacturers willing to pay significant premiums for tungsten feedstock. Morningstar

The Western Response: Emergency Diversification

Secretary of State Marco Rubio hosted delegations from over 50 countries at the inaugural Critical Minerals Ministerial in February 2026, where Washington signed eleven new bilateral frameworks and committed more than $30 billion in strategic mineral financing. CNBC The US is stepping up efforts to reduce dependence on Chinese supply through Pentagon stockpiling plans, Defense Production Act funding, and partnerships with allied producers in South Korea, Portugal, and Australia. Morningstar

The US exempted tungsten from reciprocal tariff lists — an explicit acknowledgement that penalising tungsten imports would harm domestic defence and technology industries more than it would pressure China. Cambridge Currencies Meanwhile, South Korea's Almonty Industries' Sangdong mine is expected to contribute around 7% of global supply when it ramps up in 2025–2026 — but this will not be sufficient to offset broader supply constraints. U.S. Bank Canada's Almonty Industries also announced an offtake agreement to provide tungsten oxide exclusively for US defence applications Morgan Stanley — underlining how rapidly tungsten has moved from commodity to strategic national asset in Western policy frameworks.

Alfred Vault's Perspective: Small Market, Exponential Stakes

"Tungsten is a small market — but the industries that depend on it are exponentially bigger, which is why it is on everyone's critical mineral list." Morgan Stanley That observation captures the essence of why tungsten commands our attention despite its relatively modest absolute market size.

The investment landscape around tungsten is taking shape across several layers simultaneously. Junior mining companies with tungsten assets in Western-friendly jurisdictions — North America, Australia, Portugal, South Korea — are being repriced as strategic assets rather than commodity plays. Defence contractors facing input cost inflation from tungsten price increases face margin pressure that has not yet been fully recognised in consensus earnings estimates. Processing and refining capacity outside China — currently negligible — represents a greenfield investment opportunity of genuine strategic importance. And the broader critical minerals infrastructure story — the financing, the offtake agreements, the government-backed loan facilities — is creating a new class of quasi-sovereign investment vehicle that sits at the intersection of commodity investing and defence policy.

Tungsten will not become a household name. But in the quiet arithmetic of geopolitical competition — where the difference between a functioning defence industrial base and a constrained one is measured in materials availability rather than political will — it may prove to be one of the most consequential materials of the decade. Alfred Vault is watching it closely.

This content represents the views and perspectives of Alfred Vault and is provided for informational and educational purposes only. It does not constitute investment advice. Please refer to our full disclaimer.