Rising Oil Prices, Rising Pressures: The Inflation Risk Markets Cannot Ignore

Oil does not merely power vehicles and heat buildings. It is embedded in the cost structure of nearly every good and service the global economy produces. Fertilizers, plastics, aviation, shipping, construction, pharmaceuticals — the input chains of modern civilization run through crude. For the better part of a century, this dependence was treated as a given, a stable substrate upon which consumption, trade, and growth could be planned. That assumption is now structurally in question.

The energy transition is real, but it is uneven and slow. Renewables are displacing oil at the margin, and the relationship between oil prices and consumer price inflation has eroded meaningfully since the 1970s and 1980s Investing News Network — partly due to improvements in energy efficiency, partly because the U.S. CPI basket has increasingly shifted toward services rather than goods directly tied to oil Investing News Network. Yet oil remains the single most consequential commodity for global cost structures. When it moves sharply, it moves everything — directly through energy costs, and indirectly through the second-order effects on food, freight, and manufacturing inputs.

What has changed is the policy environment surrounding oil shocks. In recent years, interest rates have become materially more sensitive to unexpected oil supply news. An oil supply surprise that typically increases oil prices by 3% resulted in two-year Treasury yields rising as much as 4.5 basis points in early 2024 — more than three times the reaction observed in the pre-2021 period. Federal Reserve Bank of San Francisco Central banks, post-2021, are far less willing to accommodate. That changes the transmission mechanism of an oil shock, and it changes the calculus for investors.

CPI inflation impact and rising oil price - Alfred vault LLC

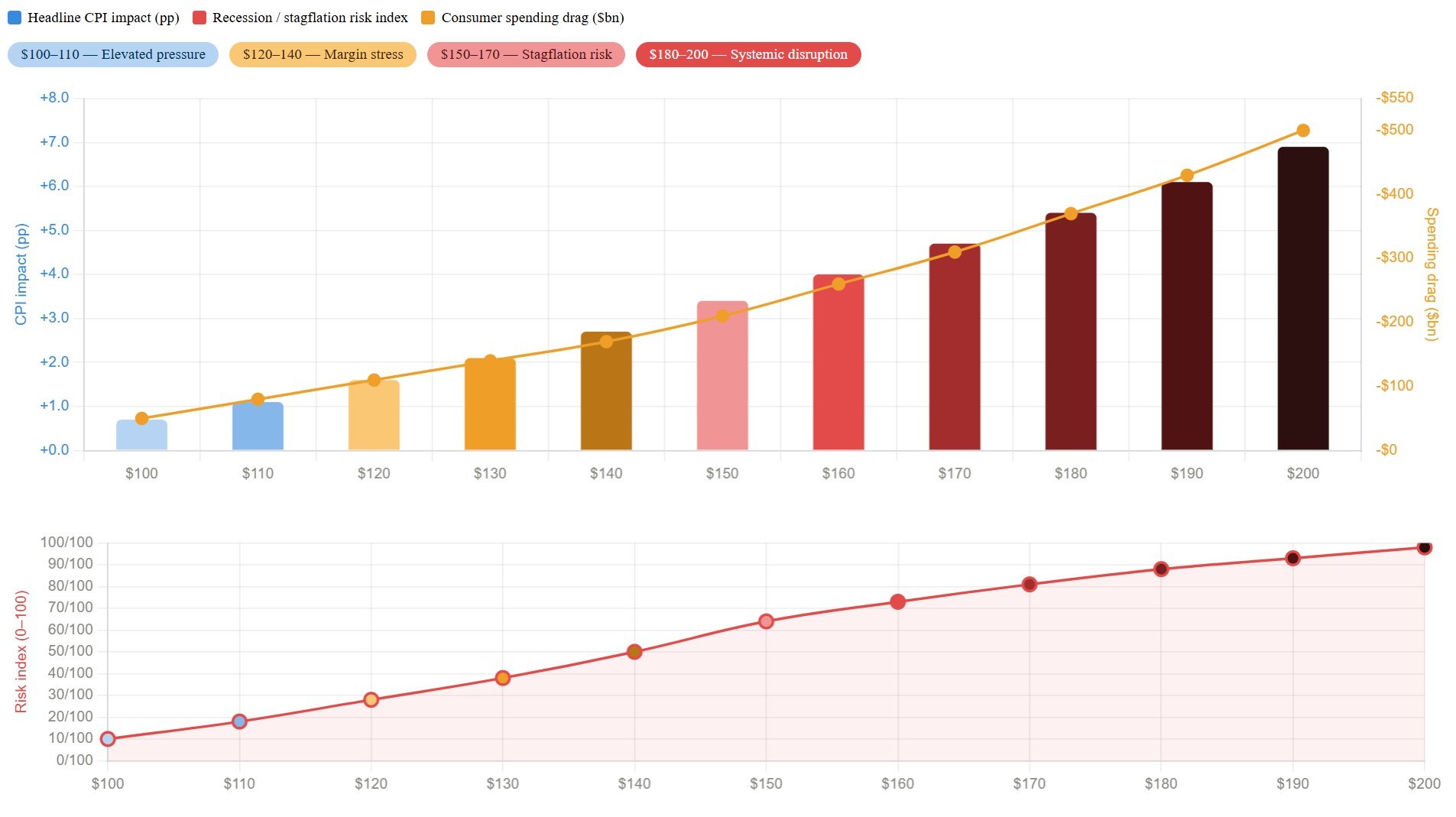

The $100 Scenario: What Markets Should Expect

One hundred dollars per barrel is not a crisis in the classical sense. It is, however, a material headwind at a moment when inflation is still above target in most developed economies. At $100/bbl — roughly $40 above the February 2026 base case assumption — headline U.S. inflation would rise meaningfully, by RBC's calculations, to above 3.5% by Q2 and remain at that level throughout the year, adding approximately 0.7 percentage points to their forecast. Each $10 increase in oil prices translates to roughly a 30-cent-per-gallon increase in gasoline prices; at $100/bbl this implies a $1.20/gallon increase — approximately a 36% rise from the $62/bbl baseline. RBC

The nominal consumer spending impact is significant: the hit to nominal consumer spending could be between $50 and $150 billion for the year depending on where WTI settles, with a more meaningful impact on lower-income consumers. RBC

At this level, central banks remain in a reactive posture but retain optionality. The dilemma is real but manageable: tighten further to suppress the inflation pass-through, or tolerate a temporary spike given still-anchored long-term expectations.

The $120 Scenario: What Markets Should Expect

At $120/bbl, the analysis shifts from household burden to corporate cost stress. The inflationary impulse becomes broad-based and harder to dismiss as transitory. Energy-intensive sectors — chemicals, freight, agriculture, airlines — face meaningful margin compression. The pass-through to producer prices accelerates, and producer prices show considerably greater sensitivity to oil price fluctuations than consumer prices ScienceDirect, meaning the pressure arrives in corporate earnings before it fully shows up in CPI.

The monetary policy response becomes more constrained. Central banks cannot credibly ignore sustained $120 oil as a "supply-side shock outside their control" when inflation expectations begin to drift. Second-round effects of oil price changes — through pass-through to food and core prices — operate with long lags and are both economically and statistically significant Federal Reserve. A sustained period at $120/bbl would feed into wage negotiations, logistics contracts, and agricultural input costs over a 6–18 month horizon, extending the inflationary episode well beyond the initial energy shock.

For equity investors, the key watch item at this level is sector rotation: commodity producers benefit, but growth-oriented and consumer-facing names face a dual squeeze from higher input costs and softening real consumer demand.

The $150–$200 Scenario: What Markets Should Expect

At $150 and above, the regime changes. This is no longer a headwind — it is a structural disruption. At $150 oil, the global economy enters dangerous territory: inflation accelerates as energy prices push up the cost of everything from food to construction materials, while economic growth simultaneously slows as consumers pull back on spending. This combination of high inflation and weak growth creates a classic stagflation scenario, placing central banks in an impossible position between raising rates to fight inflation or cutting to support growth — with neither option painless. Equipment Leases

The historical precedent is sobering. The stagflation of the 1970s, associated in the popular imagination with OPEC's oil embargo and the subsequent quadrupling of prices, led to a fundamental reevaluation of Keynesian economic policy frameworks and contributed to the rise of monetarism and supply-side economics. It took Paul Volcker's willingness to allow short-term interest rates to rise above 20 percent to finally break the inflationary dynamic — driving the economy into a sharp recession before inflation relented and recovery could begin in 1982. American Enterprise Institute

The $200/bbl scenario is qualitatively different again. It implies either a severe and sustained supply disruption — Strait of Hormuz closure, major OPEC+ fracture, or large-scale conflict in the Gulf — or a coincidence of tightening supply and surging EM demand that markets have failed to price. At this level, global recessionary dynamics become likely. Shipping costs reprice entire supply chains. Trade patterns reorganize. Capital flight from energy-importing economies accelerates. The geopolitical dimensions of energy security would dominate policy agendas. It would not be a correction — it would be a realignment.

What Investors Should Watch

The structural backdrop heading into 2026 is one of unusual fragility. Brent had already demonstrated sharp two-way volatility this cycle, and geopolitically-driven crude rallies near major energy chokepoints are likely to continue, though the underlying global market fundamentals remain soft absent a supply disruption J.P. Morgan. The base case remains well below the stress scenarios outlined here.

But the key insight for institutional portfolios is this: the transmission mechanism of oil shocks has changed. The 2021–23 inflation cycle demonstrated that even moderate and sustained energy price increases — well below $120/bbl — can produce persistent, broad-based inflation when monetary conditions are accommodative and labor markets are tight. The world today is neither as accommodative nor as tight — but it is not fully normalized either. An exogenous supply shock of sufficient magnitude would test policy frameworks that are already operating without much margin for error.

Oil is not the economy's ceiling. It is its floor. And floors matter most when the structure above begins to shift.